Solve For X

Until there is a good counterargument for cannibalization, online casino legalization will continue to be a slow slog.

The Bulletin Board

THE LEDE: Online casino supporters need better cannibalization arguments.

ROUNDUP: A look at the stories you may have missed.

NEWS: The legal rollercoaster ride that is Kalshi vs. Nevada.

BEYOND the HEADLINE: Michigan sues Kalshi; Polymarket sues Michigan.

AROUND the WATERCOOLER: Free bets in Missouri.

STRAY THOUGHTS: Being right vs. being first.

Sponsor’s Message: Increase Operator Margins with EDGE Boost Today!

EDGE Boost is the first dedicated bank account for bettors.

Increase Cash Access: On/Offline with $250k/day debit limits

No Integration or Costs: Compatible today with all operators via VISA debit rails

Incremental Non-Gaming Revenue: Up to 1% operator rebate on transactions

Lower Costs: Increase debit throughput to reduce costs against ACH/Wallets

Eliminate Chargebacks and Disputes

Eliminate Debit Declines

Built-in Responsible Gaming tools

To learn more, contact Matthew Cullen, Chief Strategy Officer, Matthew@edgemarkets.io

The Lede: iCasino Supporters Need to Solve this Problem

Virginia’s online casino bills (HB 161 and SB 118) are making progress, with the pair of bills seemingly heading for conference committee to work out the differences between the two bills.

However, even if passed, which is still far from a given, there is a big catch, as both bills now contain a reenactment clause that requires a second vote in 2027.

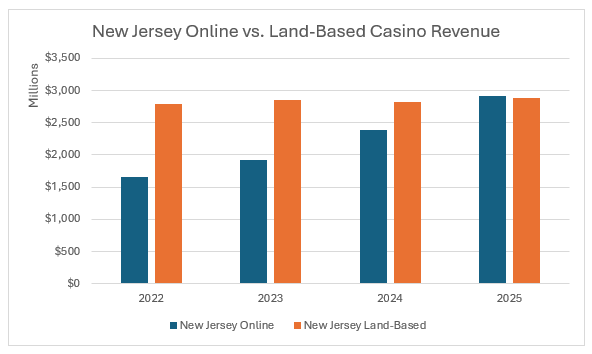

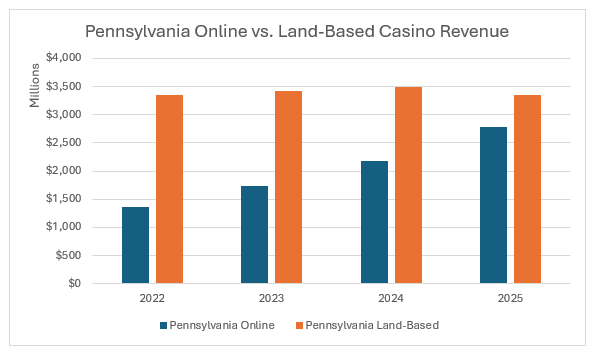

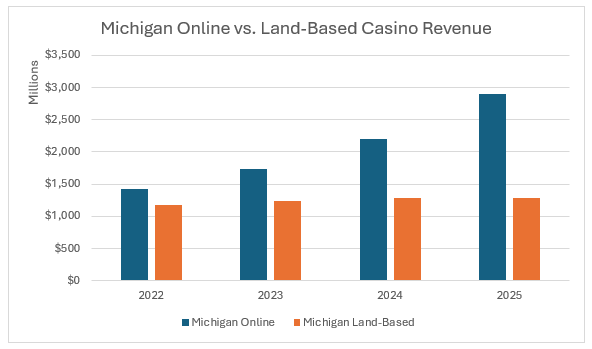

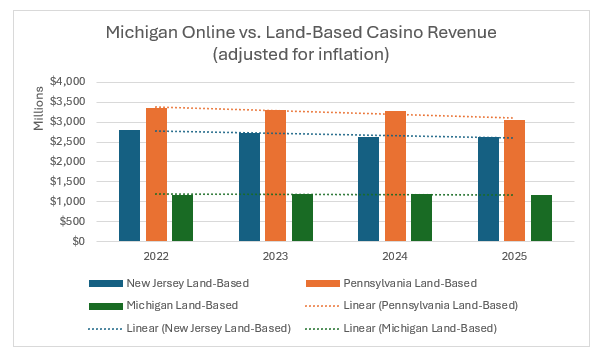

STTP believes online casino legalization will continue to flounder (with sporadic successes) as supporters have not been able to adequately explain away cannibalization concerns.

The following charts help explain some of the opposition to online casino legalization.

An even bigger issue that few people consider when they analyze historical trends is that online revenue growth is outpacing inflation, while land-based casino revenue looks far more concerning when adjusted for inflation.

And as I’ve said in the past, online and land-based revenue is not equal:

“Online deals are universally structured in favor of the online operator, who supplies the product and takes on all the risk. The license holder is, in most instances, just an access point, the holder of the key that lets you into the kingdom. The casino will typically get 5%-10% of the revenue share, maybe a bit more in some cases.

“So, not only are they concerned that land-based customers will morph into online customers (short—or long-term), but they are also concerned that when they do, the casino will lose out on their non-gaming spending and will only receive a fraction of their gaming spending as it leaks to its online partner.”

All that said, I’ll repeat another one of my thoughts:

“Still, casinos can’t stop online gambling any more than Blockbuster could stop Netflix, or Tower Records could stop streaming.

“Instead of asking how long we can preserve the current ecosystem and delay the inevitable, they should ask where they fit in. How can my organization mitigate or embrace online gambling to future-proof our business and bring in younger customers?

“The answers to those questions will differ for different properties, but complete opposition is little more than a stalling tactic. All that does is give you a stay of execution. It doesn’t eliminate online gambling or the threat it may pose to your property.”

Roundup: So Much News; So Little Newsletter Space

Missouri bill adds a second layer of sports betting taxes [Legal Sports Report]: Missouri State Rep. Jeff Knight introduced HB 3533 that adds a “24% tax on adjusted gross receipts from sports betting, which the bill defines as an operator’s revenue after paying out winnings but before any promotional costs are deducted. The tax would not replace the 10% tax on net Missouri sports betting revenue.” the bill also introduces a 1.5% access fee on remote wagering and a 13% tax on adjusted gross receipts from authorized gambling games.

Minnesota lawmakers submit new sports betting bill [Covers.com]: Minnesota has a new sports betting bill to consider. SF 4139 allows up to 11 mobile sportsbooks run through Minnesota tribes but regulated by the state. As Covers notes, “The bill also attempts to address stakeholder concerns with restrictions like banning college prop bets, limiting push notifications, excluding prediction markets from regulation, and requiring studies on gambling activity and related harms.”

Underdog cuts 20% of staff after transition to prediction markets [Front Office Sports]: “Underdog has laid off at least 125 people, including cutting two-thirds of its fraud operations team, a move that comes as the company’s focus shifts from traditional sports betting and paid fantasy draft contests to prediction markets.” Underdog CEO and founder Jeremy Levine told FOS the cuts were due to Underdog’s pivot to prediction markets. “We transitioned our business this year. We went from a focus on a state-by-state framework to a national prediction markets platform with seamless offerings across the country. It’s simply a different operation, and the changes we made are a part of that transition.”

PrizePicks to exit Canadian market [Sports Betting Dime]: PrizePicks will be ceasing its daily fantasy sports contests in Canada to focus on its newly launched prediction market product in the US. “A PrizePicks spokesperson confirmed the announcement with Sports Betting Dime. PrizePicks will no longer accept daily fantasy sports lineups or deposits by Tuesday, March 10, and will leave the country entirely by April 3. All PrizePicks users will be required to withdraw funds from their accounts by April 2.”

CFTC to begin rulemaking process for prediction markets [Reuters]: “The U.S. Commodity Futures Trading Commission will soon advance a proposal for regulating prediction markets, the agency’s Republican chairman said on Tuesday… The CFTC on Monday submitted an "advance notice of proposed rulemaking" (ANPR) to the president's budget office for review. An ANPR is the preliminary step that allows the agency to sound out stakeholders to help shape the first proposed draft of the rule.” More from the CFTC here.

Quote of the Week: “Let me be clear that if prediction markets become legal [as derivatives], no one is going to have heard of Kalshi in 10 years. It’s going to be Caesars, DraftKings, FanDuel, and MGM operating without state regulation and that is why it is an existential threat to states and tribes.” ~ Tribal gaming attorney Scott Crowell, at the Western Indian Gaming Conference

News: Kalshi vs. Nevada Is Getting Very Interesting

Kalshi has suffered another setback in its case against Nevada. Before diving into the developments over the last month, here’s a quick backstory on the case:

Kalshi filed a lawsuit on March 28, 2025, following a cease-and-desist letter from the state. US District Court Judge Andrew Gordon granted a preliminary injunction on April 9, 2025. In November, Judge Gordon reversed his earlier decision, dissolving the preliminary injunction, ordering Kalshi to halt operations in Nevada. The case is now in the Ninth Circuit, which has scheduled consolidated oral arguments for Kalshi, Crypto.com, and Robinhood appeals on April 16, 2026.

On February 11, 2026, Kalshi filed an emergency motion in the Ninth Circuit for an administrative stay to prevent Nevada from initiating enforcement actions while the appeal proceeds.

On February 17, 2026, the Ninth Circuit denied Kalshi’s request for an administrative stay in a one-sentence order, clearing the way for Nevada to proceed with enforcement. Almost immediately, the Nevada Gaming Control Board (NGCB) filed a civil enforcement action in state court seeking an injunction to halt Kalshi’s operations in Nevada, arguing that Kalshi’s sports event contracts are unlicensed gambling.

February 19, 2026: Kalshi removed Nevada’s state court action to federal court, aiming to keep the dispute under federal jurisdiction where its preemption arguments might fare better. Nevada filed an emergency motion to remand its enforcement action back to state court.

On March 2, 2026, Judge Gordon remanded Nevada’s civil enforcement action back to state court, narrowing Kalshi’s procedural options to longshot options like an emergency application to SCOTUS or an expedited stay from the Ninth Circuit to prevent the TRO from going into effect.

And as Wallach notes, the strategy for states seems pretty clear:

“The [Nevada] remand order could embolden other states to emulate the Massachusetts (and now Nevada) strategy of suing Kalshi in state court in lieu of sending cease-and-desist letters. States are undefeated (3/3) in state court civil enforcement actions.

“Kalshi's attempt to remove these cases to federal court will be short-lived (see MA and NV) because the removing party must meet the higher bar of "complete preemption" to avoid remand; a general preemption argument (i.e., field, express or conflict preemption) will not suffice.

“Only 3 federal statutes have ever been found by the U.S. Supreme Court to ‘completely preempt’ state laws -- and the Commodity Exchange Act s not one of them.”

Sponsor’s Message: Promoting a sustainable, entertainment-first global gaming industry.

Play’n GO is celebrating its 20th anniversary in 2025. Drawing on that experience from the dawn of the iGaming industry through to today, Play’n GO designs and creates world-class slot games in the online casino space.

Play’n GO wants to see a sustainable industry that puts players first. To realize that vision, Play’n GO:

Creates games designed to be entertaining and fun first

Actively lobbies for increased regulation to keep players safe

Refuses to make games that feature mechanics that we believe to be predatory, such as those that allow players to pay hundreds of times their normal stake to buy into the bonus round directly (‘Bonus Buy’ games)

Now live in over 35 regulated territories around the world, including all US and Canadian iGaming jurisdictions, Play’n GO is the leading provider of entertainment to the online casino industry.

For more info, visit www.playngo.com

Beyond the Headline: Michigan Preemptively Sues Kalshi

The playbook (created by Massachusetts) for states trying to prohibit prediction markets from offering sports contracts within their borders seems pretty clear, yet few are following it.

As attorney Daniel Wallach explained here, the path is much clearer in state court:

“The [Nevada] remand order could embolden other states to emulate the Massachusetts (and now Nevada) strategy of suing Kalshi in state court in lieu of sending cease-and-desist letters. States are undefeated (3/3) in state court civil enforcement actions.

“Kalshi’s attempt to remove these cases to federal court will be short-lived (see MA and NV) because the removing party must meet the higher bar of “complete preemption” to avoid remand; a general preemption argument (i.e., field, express or conflict preemption) will not suffice.

“Only 3 federal statutes have ever been found by the U.S. Supreme Court to ‘completely preempt’ state laws -- and the Commodity Exchange Act is not one of them.”

But there is at least one state paying attention: Michigan.

On March 3, 2026, Michigan Attorney General Dana Nessel filed a civil enforcement action against Kalshi in Ingham County Circuit Court, accusing Kalshi of operating an unlicensed gambling platform.

Perhaps seeing the writing on the wall, Polymarket preemptively sued Nessel and Michigan Gaming Control Board in federal court the following day. Polymarket contends that as a federally regulated entity under the Commodity Futures Trading Commission (CFTC), it is exempt from state gambling regulations, citing the Kalshi lawsuit as evidence of an “immediate threat.”

Around the Watercooler

Social media conversations, rumors, and gossip.

This series of tweets seems important:

Recall what I recently said about the nonsensical use of handle earlier this week:

“Normally, someone depositing $100 will win about half their bets and lose half their bets. That leaves them with half their original deposit to bet again, and the process repeats until they go down to zero. Their $100 deposit might get “recycled” 2-3 times before that happens, resulting in $200-$300 in handle.”

Now, think about how much handle is generated when a customer is given several hundred dollars of bonus money and bets on top of that same $100 deposit.

Stray Thoughts

I often have these same thoughts with gambling reports, and the rush to add “Breaking” or “Exclusive” to a story or tweet.

For me, it’s more than being correct; it’s adding something of value to the conversation. If 10 people are going to relay the same news within minutes of one another, I’d rather wait a day and add something of interest/value to the conversation than beat them by a few seconds. Breaking news is great, but are you really “breaking news” because you hit send faster than someone else?

The real issue is how land casino operators retain the lion's share of the economics from online casino. Unlike sports betting, national and regional casino brands have done extremely well in hypercompetitive online casino markets, hanging on to over 50% of the market for years, with much more favorable demographics than the male-dominated sports-led digital juggernauts.

Regional casinos that offer both sports and casino make 10X more revenue from online casino. With an experienced core iCasino team and a good B2B technology platform they can offer a market-leading product, unlike sports betting where the giants have a massive head start in math models for in-play betting and same game parlays.

While there is a consumer argument for allowing an open competitive market in sports betting, it's less obvious that land casino licensees who employ thousands of local people should see half the online casino market captured by digital natives with a negligible in-state footprint.

Either way, ignoring the issue won't make it go away. While the primary cannibalization threat for land casinos will always be other land casinos, as Atlantic City knows, if the global experience of retail and online wagering over the past 20 years is anything to go by, pretty much all the growth over the next decade in the US will be online. Land casinos can adapt and capture a younger omnichannel demographic who still value IRL experiences like a night out at their local casino, but they can't stem the tide of innovation.